IRS Streamlined Foreign Offshore Procedures

In this post:

- Streamline Foreign Offshore Procedures (SFOP) – Overview

- Eligibility for SFOP

- Requirements of SFOP – Checklist

- Who should not use SFOP!

How can Maroof HS CPA Professional Corporation help with streamlined foreign offshore procedures?

Internal Revenue Service (IRS) has strict rules when it comes to filing your taxes. You have to report all your income, and foreign assets and provide all applicable information to support your returns. All American Citizens living in Canada must file their US taxes every year.

The inability to file your taxes or report foreign assets where needed can be disastrous. You can invite trouble from the IRS which may include tens of thousands in penalties and even criminal prosecution.

How can US taxpayers come clean and clear things with the IRS? What if you have missed filing tax returns, FBARs, or other information returns in the past years?

What if the returns are inaccurate, missing information slips, or contain errors?

The answer to all these questions can be Streamlined Foreign Offshore Procedures. It is a safe way to correct non-compliance with U.S. tax laws. Additionally, you may not have to pay heavy penalties that generally apply to defaulters.

What Are Streamlined Foreign Offshore Procedures?

The Streamlined Foreign Offshore Procedures are offered by the IRS for specific taxpayers. It allows them to file certain numbers of tax returns, information returns, and FBARs to correct the past non-compliance.

Most importantly, the taxpayer does not have to pay hefty penalties for not filing certain information returns on time.

Individual taxpayers must meet the eligibility criteria to take advantage of Streamlined Foreign Offshore Procedures. We will discuss them in the next section.

Streamlined Foreign Offshore Procedures protect the taxpayer from penalties for various acts like:

- Failure-to-pay penalties

- Failure-to-file penalties

- Penalty for inaccuracies

- FBAR penalties

- Information return penalties

Eligibility for Streamlined Foreign Offshore Procedures

US taxpayers will have to satisfy two primary criteria to be eligible for Streamlined Foreign Offshore Procedures:

- They will have to fulfill specified non-residency requirements. For joint filers, spouses of taxpayers should satisfy the non-residency requirements too.

- Forgot to report their foreign income from financial assets and file taxes or were not able to file an FBAR related to any foreign financial account

In all cases, all failures should arise from non-willful conduct. It is important to note that a taxpayer may have non-willful conduct and not file taxes due to negligence.

It may also be even due to a mistake that was unintentional and resulted from not understanding US tax laws.

Now, let’s take up the first eligibility in detail to get a clear picture.

Non-residency Requirement for Streamlined Foreign Offshore Procedures

Taxpayers have to fulfill non-residency requirements for Streamlined Foreign Offshore Procedures. It means they must be a foreign resident.

However, a foreign resident may have varying statuses based on:

- Whether they are a US citizen

- Whether they hold a Green Card

- Whether they are a non-US citizen or Green Card Holders

Us taxpayers and Legal Permanent Residents should satisfy the 330-day rule to be eligible as a foreign resident.

- The individual taxpayer should not have a U.S. abode.

- It mandates them to spend a minimum of 330 days outside of the United States in any of the past three years.

- The above 330 days test should include the period for which the U.S. tax return filing date has passed.

However, the taxpayer may visit or stay in the US temporarily if they fulfill the 330-day rule. Additionally, any lodging the person owns in the US may not qualify as a US abode.

You can read the IRS Publication 54 for the definition of a US abode and see if you qualify for it.

Examples of Non-Residency

Don’t live in Canada all through the year? We will go over a few examples to illustrate the eligibility for being a foreign resident.

Scenario 1. Miss Teressa took birth in the US but left for Canada with her mother and father. She lived in Canada and never had an abode in the US.

In this case, Miss Teressa satisfies the non-residency requirement as a US citizen.

Scenario 2. Let’s imagine everything is the same as in the above example. However, Miss Teressa traveled back to the United States and bought a US abode in 2017.

Therefore, Miss Teressa was outside the US in 2015, 2016, and 2017. As a result, she will satisfy the non-residency requirement.

Non-Residency Requirement for Non-US Citizens or Non-lawful Permanent Residents

Non-US citizens or people who are not lawful permanent residents will also have to fulfill the non-residency requirements. People who are estates of persons who are not US citizens should also fulfill the non-residency requirements.

They might claim non-residency if they did not pass the substantial presence test. It is presented by IRS section 7701(b)(3).

The IRS Publication 519 has information on the substantial presence test. You can visit the link for more information.

Scenario 3. Miss Julia is not a lawful permanent resident or citizen of the US. She was born in Canada and stayed there till April 1, 2019. Next, she arrived in the US with a job transfer from her country.

Therefore, Miss Julia resided in the US for over 183 days in both 2019 and 2020. Her due dates for filing taxes were also in 2018, 2019, and 2020, the last three years.

As a result, Miss Julia satisfies the substantial presence test for 2019 and 2015. However, she was not able to pass the test in 2018.

Therefore, Miss Julia will fulfill the non-residency requirement meant for non-US citizens or non-lawful permanent residents.

Checklist for Filing Streamlined Foreign Offshore Procedures

Now, we will find out how you can take advantage of the Streamlined Foreign Offshore Procedures.

If you qualify for the procedure, you will have to follow the steps below:

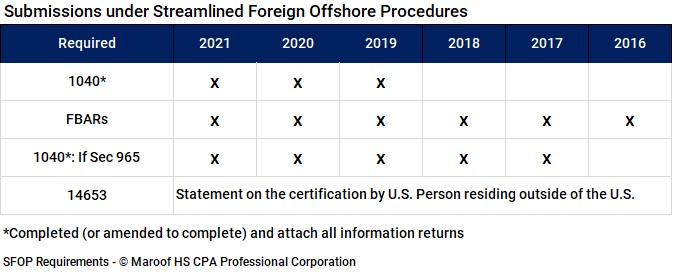

File 3 Most Recent Tax Returns and Information Returns

File the most recent three amended or delinquent ‘completed’ tax returns for which the due dates have been passed. Additionally, you should provide ‘all’ information returns like:

- Form 8938

- Form 5471

- Form 3520

File 6 Delinquent FBARs

You should file the most recent 6 delinquent FBARs for past due dates. You can file it using the FinCEN Form 114.

Check out the FBAR instructions when you file your delinquent FBARs. You should also include a statement explaining your filings are under the Streamlined Filing Compliance Procedures.

You may visit the FinCEN link to file your delinquent FBARs electronically. Choose the “other” option when the digital form asks you for a reason for late filing.

Then, an explanation box will appear where you need to provide Streamlined Filing Compliance Procedures.

Be sure to remit all taxes and due interests with your amended filings

Taxpayers can avoid penalties for non-willful mistakes and failure to file taxes using these procedures. The IRS will not charge them with failure-to-pay and failure-to-file penalties.

Additionally, they may prevent paying for accuracy-related penalties. Moreover, the IRS will not levy any FBAR penalties or information return penalties.

Most importantly, taxpayers can avoid all the above penalties even if their filings are subjected to audits.

However, you may attract a penalty if the IRS finds your filings to be fraudulent. Remember, the IRS may charge a penalty if your FBAR violation was willful, it must be non-willful.

Do note that you will have to pay any past penalties levied by the IRS in your amended returns. Moreover, the IRS may audit your filings to find out if there is any deficiency. If the IRS finds any deficiency, it may charge additional taxes or levy penalties.

Sign a Non-Residency Statement

You will have to provide a statement to certify that you have been living outside the US. You can use Form 14653 to certify your status.

The statement certifies that:

- You qualify for the Streamlined Foreign Offshore Procedures

- You have filed all the necessary FBARs

- You also certify that any non-filing of returns or error is due to non-willful conduct

You should sign and submit the original document. Along with that, you include the statement for all information returns and tax returns you are filing under the procedure. The statement must provide the details of all the favorable and unfavorable circumstances.

However, you do not need to provide copies of FBARs that are filed electronically.

The returns must be properly marked, otherwise, the IRS will process your returns under regular circumstances, and you may have to pay penalties.

Pay Your Taxes and Interests

Now, you must pay all applicable taxes calculated on your returns. You should also pay any statutory interest applicable for missing your due dates and late payments.

Additionally, don’t forget to write your taxpayer identification number on your check. It will help the IRS charge any additional amount or refund your money.

Note: Some taxpayers may not have a taxpayer identification number or ITIN. In such cases, you should submit an application for your ITIN with your current filings. If you do need ITIN, get in touch with us.

The tax returns under Streamlined procedures cannot be electronically filed and must be submitted in paper forms.

Who Should Not File the Streamlined Foreign Offshore Procedures

The Streamlined Foreign Offshore Procedures are for non-willful, though negligent, violations only. You will have to mention the specific reasons behind your unintentional failure to file taxes or inaccuracies.

The IRS will scrutinize your reasons and documents to find out if your violation is really non-willful. Therefore, don’t file the Streamlined Foreign Offshore Procedures if your violation is intentional. It can invite serious trouble and even penalties from the IRS.

So, people who have willfully avoided taxes or changed the numbers should choose another process. For intentional or willful non-compliance, you may be eligible for Offshore Voluntary Disclosure Program (OVDP).

Your filings should be accepted by the IRS if you followed all the steps and provided accurate information. You can now pay your pending taxes and even avoid hefty penalties.

However, a cross-border tax accountant can reduce challenges and make the process easier for you.

Alternatives to Streamlined Foreign Offshore Procedures

There are a couple of other options that can be used either to avoid or minimize the substantial penalties attached to international information returns. Some of them are:

- Delinquent FBAR Submission Procedures: Where tax returns do not require amendments and the only non-compliance is related to FBAR.

- Delinquent International Information Return Submission Procedures (DIIRSP): To submit delinquent international information returns such as 5471, 5472 or 3520 etc. May require a reasonable cause statement!

- Offshore Voluntary Disclosure, for willful non-compliance

Almost all of the above requires that the taxpayer is not under audit, examination, civil or criminal investigation.

How Can We Help?

We can help you with:

Preparing Your Tax Returns and Information Returns

SFOP requires complete three years of U.S. tax returns (or amended ones). All the required information returns must be prepared and attached to tax returns. Where Section 965 transition is involved, tax returns are required since 2017.

We prepare all the tax returns (or amended tax returns) along with all required information returns.

Filing Delinquent FBARs

You are required to file six past delinquent FBARs under SFOP. We help you gather the required information, prepare all FBARs and submit them as per the strict instructions.

Assistance with Creating Statement

You will have to present a statement to certify your non-residency status and provides details of the circumstances. This statement must meet set criteria. If needed, we involve a tax attorney trusted and tested by us so that you can get the best advice.

Our team can also provide solid guidance on associated tax matters. We might even find you opportunities to save taxes if it is possible.

So, contact us today to file your taxes under the Streamlined Foreign Offshore program.

Disclaimer: This post contains a very high level and limited information for the taxpayers looking to correct the non-compliance. A must-read guide from IRS is here. You must consult a professional cross-border tax accountant with streamlined offshore procedures. Get in touch with us to see how can we help you.