Non-residents of Canada face some challenges when it comes to compliance when owning Real Estate in Canada. Non-Residents here does not mean Non-Canadians, it also includes Canadian citizens and permanent residents who emigrated from Canada.

In recent years, due to the housing crisis in Canada, all levels of government have taken different measures to discourage non-resident ownership. Recent changes in tax laws such as the Underused Housing tax or Prohibition on the Purchase of Residential Property by Non-Canadians Act, all aim to address the housing crisis.

This article addresses the Non-residents of Canada selling Canadian real estate properties only. The certificate of compliance under section 116 is required when a non-resident of Canada disposes of a taxable Canadian property (TCP). TCP does not include Canadian real properties only, however, in this article we are limiting the discussion to the dispositions of Canadian real properties only. Further, this article is for general informational purposes only, and does not cover all the possible tax issues involved for all the taxpayers. Non-residents of Canada must consult their professional accountant specializing in certificates of compliance.

A quick overview

When a non-resident of Canada owns a real property, the compliance requirement depends on the use of the property. Based on the use of that property compliance requirements can vary.

In general, there are three major requirements to comply with the tax laws:

- Rental income – Part XIII withholding taxes and Section 216 Income tax returns

- Underused housing tax returns to be submitted by certain affected owners. UHT-2900 returns, if needed, must be filed forthe 2022 to 2024 tax years.

- Certificate of compliance to report disposition of a Canadian real property by a Non-resident of Canada, this article discusses this

Please note that the above three key compliance areas are related to income tax compliance only. Different municipalities have their own requirements, for example, the city of Toronto’s Vacant Home Tax

Read: Infographic – A compliance overview for the non-residents of Canada owning Canadian Properties

Section 116 – Certificate of Compliance

The legislative authority for the Certificate of Compliance requirement while disposing of Canadian real property originates from Section 116 of the Income Tax Act (ITA). The purpose of ITA section 116 is to ensure that the non-residents of Canada fulfill their income tax obligations in Canada.

Who must apply for a Certificate of Compliance?

Any non-resident of Canada, including non-individual taxpayers, must apply for a certificate of compliance while disposing of a Taxable Canadian Property (TCP). TCP is a much broader and slightly complex area, however, this article is limited to Canadian real properties only.

A Canadian real property is always a Taxable Canadian Property. Even shares of a corporation (not listed on a stock exchange) that derive more than 50% of their value from real or immovable property are also TCP.

Non-residents of Canada include individuals who are non-residents or deemed non-residents of Canada for tax purposes; corporations and entities such as Partnerships and trusts. If the property is owned by more than one person, each non-resident must apply for the certificate of compliance. For example, a joint property owned by two spouses will require two certificate of compliance requests if both of them are non-residents of Canada. If one of them is a resident of Canada and the other one is a non-resident, only the Non-resident spouse needs to apply.

When and How to Apply?

Any non-resident selling Canadian real property must notify within 10 days of the disposition. Failure to notify the CRA within 10 days of disposition results in penalties. The penalty is $25 per day, a minimum of $100 and a maximum of $2,500 per certificate of compliance.

The notice as described in the ITA Sec 116 is sent by registered mail, or online, on the prescribed forms by the CRA. The CRA has two different forms for this purpose.

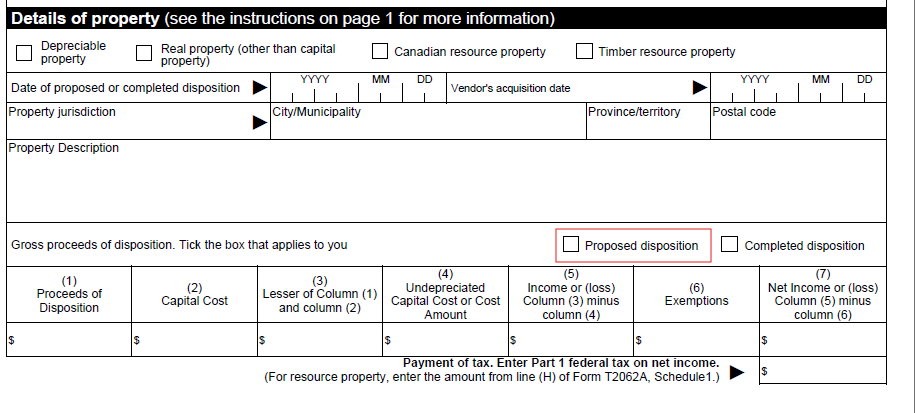

- Form T2062 – Required for all real property dispositions

- Form T2062A – Required if the property sold was a rental property

These forms require further supporting documents about the transaction, property disposed off, proceeds of dispositions and adjusted cost basis.

Payment requirement

Both T2062 and T2062A must accompany the tax payment calculated on these forms.

- Capital gains calculated on T2062 require a tax payment to be attached that is equal to 25% of Capital gains

- Net income calculated on T2062A, basically a recapture of the CCA claimed, requires the payment to be attached equal to the Part 1 federal tax on that income

Capital gains referred to here do not include selling expenses. Of course, selling expenses reduce the income taxes, however, they can be claimed by filing a tax return after a certificate of compliance is issued.

How much is withholding?

As Section 116 imposes penalties in the form of purchaser’s liability, the purchaser’s lawyer must withhold from the proceeds of disposition:

- 25% if the property was never rented

- 50% of the proceeds when the property disposed of generated rental income

These withholdings are often more than the payments required for the capital gains.

A practical tip is to request the purchaser’s lawyer remit to CRA from the trust account the amounts calculated on T2062 and T2062A.

Further, it’s always smart to request a comfort letter while applying for this certificate of compliance. CRA will issue a notice to pay if the tax amount is not attached to the notification. You can always advise the lawyer to remit as per the notice-to-pay.

Proposed Vs Completed Disposition

Requesting a certificate of compliance is a time-consuming process. CRA takes a few months to process these requests. There may be a reason to start the process earlier than the closing of the property to minimize the impact on the cash flow.

Section 116 allows the notification process for both completed and proposed dispositions.

- Completed dispositions are for those real properties where the sale or transfer of the real property by the non-resident is finalized.

- A proposed disposition refers to the intention or plan of a non-resident to sell or transfer taxable Canadian property.

Requesting a certificate of compliance for a proposed disposition may result in having a certificate of compliance issued before the closing date and avoid withholding requirements. If the proceeds of disposition under the proposed disposition are less than the actual proceeds, the purchaser’s lawyer will still withhold taxes on the difference in amounts.

Proposed dispositions also require the payment of tax or an acceptable security to be attached to the requests.

Some possible situations where the payment of tax may not be needed while requesting a certificate of compliance under the proposed disposition:

- An emigrant from Canada who is selling the real property after moving out of Canada and the property was a principal residence at the time of emigration. This can be particularly helpful in avoiding a cash crunch resulting from the withholding.

- Real properties that have dropped in value and are expected to sell at a loss.

Some Select Issues and Challenges

How to avoid Sec 116 withholding?

Can I avoid withholding when I sell Canadian real property as a non-resident? No.

Section 116 imposes penalties on the purchase of real property. It is extremely rare that a lawyer is not aware of these withholding requirements.

As you cannot avoid the withholding, the cashflow crunch can be resolved by planning ahead of time. You can apply using the proposed disposition well ahead of the closing.

Certificate of Compliance – Gift of property

It is common for a non-resident of Canada to transfer a real property to a Canadian resident.

When a non-resident of Canada transfers a real property, the notification requirements under Section 116 still apply. In Canada, the person who transfers the property (transferor) is responsible for paying the taxes on Capital gains. Such a transfer must be done at the fair market value.

In such non-cash transactions, a fair market valuation (FMV) in the form of an opinion letter is needed. The difference between the FMV and the adjusted cost basis result in the Capital gains. If eligible, the non-resident can use their principal residence exemption or other adjustments to the cost basis to reduce the impact of income taxes.

The transferee must also be aware of the consequences of the consideration mentioned in the agreement. A consideration less than fair market value will still require the capital gains to be calculated at FMV for the transferor but the cost basis of the transferee is equal to the consideration mentioned only. It is very common for unsuspecting transferee of real properties to use ‘o’ consideration to avoid land transfer taxes. This does not avoid capital gains taxes for the transferor but the transferee loses the cost basis.

Non-residents cannot claim principal residence exemption unless they meet certain criteria!

Certificate of compliance – Emigrating from Canada

Canadian real properties are not subject to departure tax in Canada unless an election is made on form T2061A. An emigrant from Canada does not need a certificate of compliance.

If an emigrant sells or transfer the Canadian real property after moving out of Canada, they must request for a certificate of compliance. If the property was a principal residence at the time of emigration, ideally they should elect the deemed disposition at emigration and shelter the capital gains using principal residence exemption. Once they become non-resident of Canada, they cannot designate the same property as a principal residence unless certain criteria are met. In all cases, principal residence exemption is not available for the ownership period during non-residency in Canada.

Unfiled Section 216 or past tax returns

If you rented your property while a non-resident of Canada, Part XIII withholding taxes on gross rental income are applicable. Section 216 allows you to calculate the income taxes on rental income by taking deductions. Section 216 tax returns must be filed within two years from the end of a tax year, or 6 months if NR6 was filed. Failing to file Sec 216 tax returns within this time period results in a loss of ability to claim the deductions.

There is a CRA’s administrative policy that still allow late filing of section 216 tax returns for first-timers beyond this two-year limit.

Since the Underused Housing Tax (UHT) came into effect, annual filing for certain affected owners is mandatory which may result in taxes. Such UHT-2900 returns must be filed as well.

If you are in a situation where you have not previously filed Section 216 tax returns and require a Certificate of compliance, get in touch with us.

Ensure Form T2062 and T2062A are complete

Requesting a certificate of compliance involves processing time over a few months. It is important that both forms T2062 and T2062A are complete and have all the supporting documents attached.

- Adjusted cost basis requires careful consideration. A miscalculation or missing supporting documents can result in the denial of the relevant cost that can result in additional tax owing.

- Errors in calculation of adjusted cost basis, for example, ignoring the bump in basis at emigration, or capital improvements can cause additional tax owing. (very common)

- Opinion letters on the FMV of properties are needed. These letters need to be worded carefully and must be issued by licensed real estate agents.

- Principal residence exemption worksheets and forms must be completed and attached.

- If you were claiming CCA on the rental properties, you must attach all the CCA schedules from past tax returns. Recapture of CCA and Part 1 federal tax must be calculated correctly and carefully.

- Documents related to sales and purchase transactions must be attached

- Must be sent through registered mail, CRA my account or by a professional accountant Rep-a-client

Filing a Tax Return to claim a refund

As mentioned before, the certificate of compliance does not take into account selling expenses while calculating capital gains.

Once the certificate of compliance is issued, a tax return under Section 116 is filed to report this disposition. On this tax return, you can claim selling expenses resulting in a refund. Since the selling expenses are often around 5% of the proceeds, this can result in a significant amount of the refund.

How Can we help?

Maroof HS CPA Professional Corporation assists with full-scale income tax compliance for non-residents. We can assist with the submission of requests for certificate of compliance, and preparation of section 216 tax returns and UHT-2900 returns, and are capable of handling complex tax issues involved.